On 5 October OPEC+ announced that it would cut oil quotas by 2.0 million barrels per day (mbpd) from November. The cut will be the largest since 2020, representing around 2% of global oil output.

The OPEC+ cut signals to the rest of the market that the cartel intends to put a floor under crude prices—halting the bear market that had overtaken crude since June. The cut also comes just as crude releases from the U.S’ Strategic Petroleum Reserve are to end in October, and as the EU’s ban on seaborne imports of Russian crude is to take effect from 5 December.

The move will keep oil prices higher for longer. That said, the quota cut is unlikely to lead to a prolonged rebound in prices from their current level of slightly below USD 100 per barrel. To begin with, OPEC+ members have been consistently undershooting their quotas in recent months. As such, the actual hit to production will likely be around 0.9 mbpd, mainly affecting the production of Kuwait, Saudi Arabia and the UAE. In addition, the global economy continues to slow, dragging on crude demand, with the heads of the IMF and World Bank recently warning about the rising risk of a global recession.

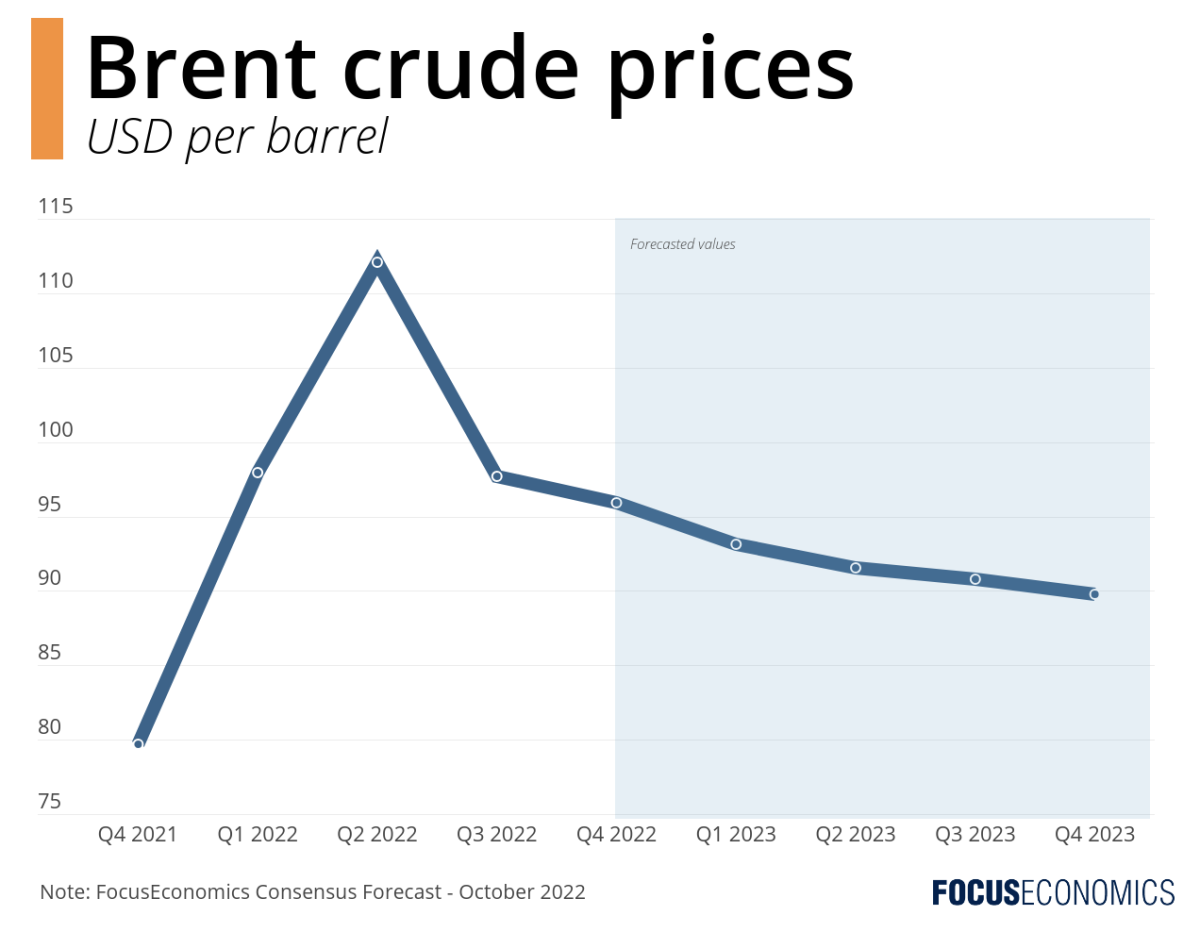

Our panelists see prices remaining roughly stable in Q4 2022 at 95.9 per barrel. Prices are then projected to dip gradually next year and average 89.8 per barrel in Q4 2023. Key risks to the outlook include a G7 price cap on Russian oil, a potentially sharp rebound in Kazakhstan oil output as maintenance and repair work finishes, and an Iranian nuclear deal. Regarding the G7’s plan, member states will prohibit banking, insurance and shipping firms from providing services to Russian firms that sell crude at a price which exceeds the yet-to-be-defined price cap. However, if the Kremlin refuses to play ball, large quantities of Russian crude could be shut out of the global market, raising global prices.

-

Insights from our analyst network:

TD Economics’ Jenny Duan commented on the outlook following the announcement:

“The global macroeconomic backdrop continues to weaken amid increasingly hawkish monetary policy. For oil markets, higher prices in the near term could mean increased demand destruction in 2023. We maintain the view that despite any near-term rallies, there is limited upside potential for prices heading into 2023.”

Analysts at Fitch Solutions commented on risks to the now more bullish outlook:

“Brent’s [recent] breakout from its multi-month downtrend is a positive sign for the group and, from a fundamental perspective, there are reasons for optimism. However, oil market sentiment remains fragile and, should prices relapse below USD 90 per barrel after such a sizeable cut, the group’s credibility could be damaged. Any loss of faith in the OPEC+ ‘put’ would be extremely bearish for prices and poses a downside risk to our current forecast for Brent crude to average USD 100 per barrel next year.”