Furthermore, the Bank sees the political landscape as another potential threat to the inflation outlook. Political uncertainty surrounding several issues, including the impact of potential court-ordered payments on the 2022 budget and an increased willingness to boost government spending during an election year, threaten to weigh heavily on policy credibility and financial stability.

Looking ahead, despite significant slack in the labor market, drought and frost wreaking havoc on the agricultural and utilities sectors, and ongoing uncertainty surrounding the Covid-19 crisis, the Central Bank seems set on tamping down price pressures. Our panel of analysts sees inflation averaging higher in H2 relative to the first half of the year, and expects economic activity to expand moderately in sequential terms for the remainder of 2021.

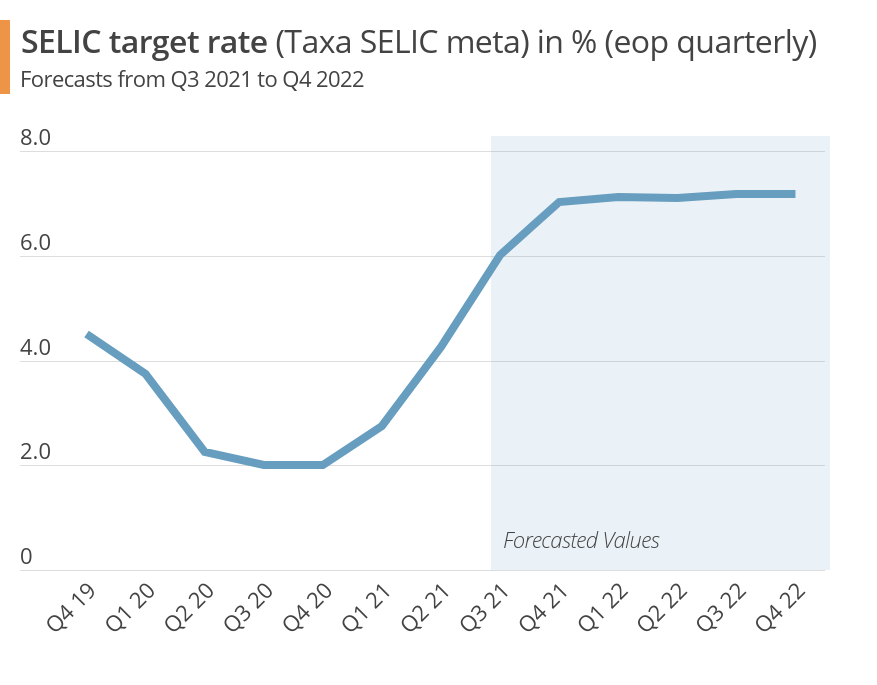

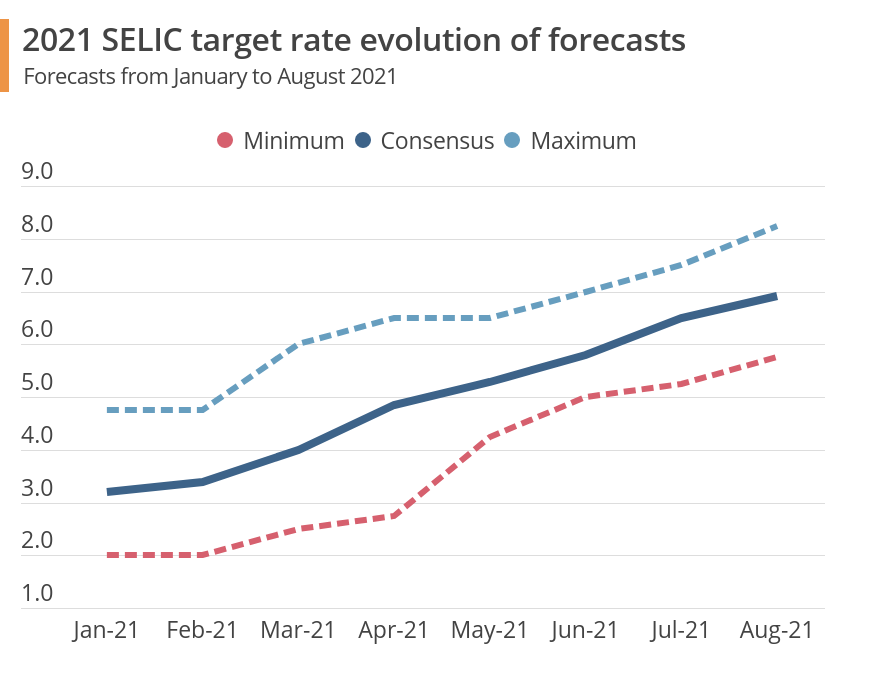

Consequently, our FocusEconomics Consensus Forecast is calling for further tightening from the Central Bank before year-end, but the forecast spread is wide. The minimum projection calls for a 50 basis-point increase to the SELIC rate by the end of 2021, while the maximum is for an increase of 300 basis points by year-end. This puts our Consensus Forecast at a staggering 6.98% for 2021. Our panel is relatively split on further tightening next year, with our Consensus Forecast seeing the SELIC rate ending 2022 at 7.13%.

Consequently, our FocusEconomics Consensus Forecast is calling for further tightening from the Central Bank before year-end, but the forecast spread is wide. The minimum projection calls for a 50 basis-point increase to the SELIC rate by the end of 2021, while the maximum is for an increase of 300 basis points by year-end. This puts our Consensus Forecast at a staggering 6.98% for 2021. Our panel is relatively split on further tightening next year, with our Consensus Forecast seeing the SELIC rate ending 2022 at 7.13%.

Insights from Our Analyst Network

Commenting on recent policy developments and monetary policy, analysts at JPMorgan noted:

“The perception of a broader deterioration in the policy mix has led to a significant financial tightening. Lack of credibility of economic policy continues to push up inflation expectations, which led markets to price another pickup in the pace of tightening to 125bp at the next COPOM meeting. While we continue looking for a 100bp hike at the next meeting, in line with committee members’ recent communication, we recognize that the risks of a more prolonged 100bp pace cycle are rising. […] In our view the recent indications of a shift to an easier fiscal policy have been counterproductive, pressuring monetary policy and weighing on 2022 growth prospects.”

Commenting on the inflation outlook, analysts at the EIU noted:

“We expect inflation to soon ease and converge towards the declining medium-term midpoint targets. Disinflation will be the result of monetary policy tightening, combined with a persistent output gap and a slackening in producer price inflation. […] However, there are clear risks to this outlook if inflation expectations become unanchored. […] If the government’s commitment to fiscal consolidation wavers, or if the global inflation picture were to deteriorate amid supply shortages, a more persistent inflationary problem could emerge.”

Our Latest Analysis

Central bank interest in cryptocurrencies is rising. In our latest insight piece, we examine the current state of central bank digital currencies (CBDCs) and what they could mean for the economy.

Business activity continued to expand at a relatively strong pace in August. Our senior economist Massimo Bassetti has the latest.