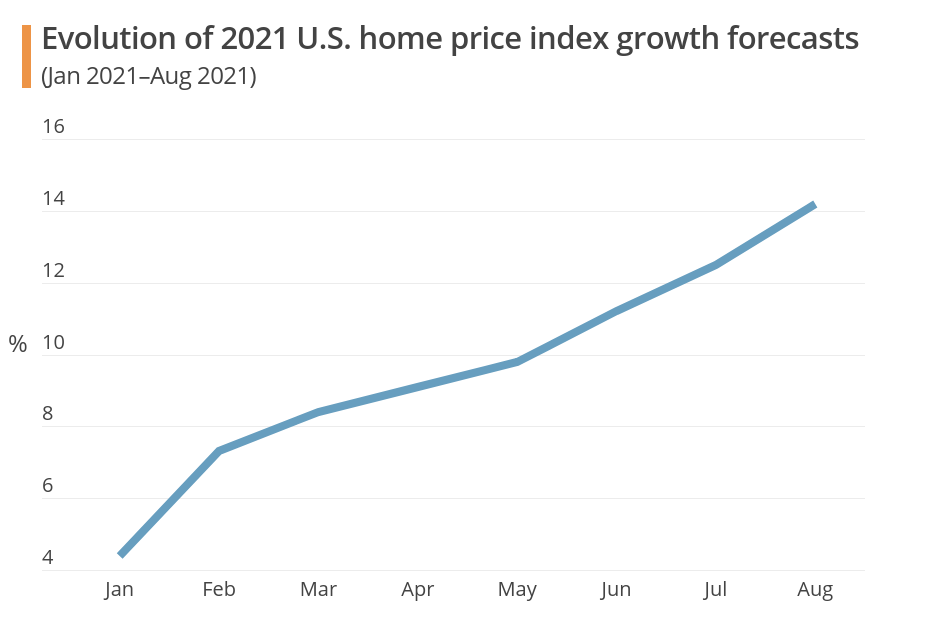

Although supply levels will likely remain tight for the remainder of the year, the housing market should cool ahead as potential buyers are priced out. Our panel of analysts have gradually hiked their forecasts for home price growth since the start of the year and now expect prices to rise 14.2% in 2021—the highest level of growth since 2005—and 6.5% in 2022.

Elevated house prices will have severe implications for inflationary pressures for the remainder of 2021 and into 2022. Inflation was stable at June’s 13-year high in July, and while the Fed has deemed recent price pressures to be largely transitory, rising housing costs could keep inflation running above 2.0% well into next year. This could force the Fed to speed up its timeline for tapering its QE program and potentially raise rates amid the ongoing labor market recovery and strong domestic growth

Insights from Our Analyst Network

Commenting on home price growth and what it means for inflation and interest rates, James Knightley, chief international economist at ING, noted:

“Primary rents and owners’ equivalent rent account for a third of the CPI basket and […] movements in these components tend to lag 12–18 months behind the S&P Case Shiller house price series. […] If we see the CPI housing costs merely move from 2% yoy to 4% yoy, that on its own will be enough to add 0.7 percentage points to headline inflation […]. This is a key story why we expect headline inflation to remain well above 4% through Q1 2022 with core inflation persisting above 3.5%. Such an outcome would […] add more momentum behind the case for earlier interest rate increases.”

Commenting on July’s inflation report, Leslie Preston, senior economist at TD Economics, noted:

“As expected, many of the re-opening-related price spikes seen through the spring have started to cool. […] However, other key categories are showing that inflation pressures in an economy running at a 6%+ pace in real terms are not gone. Namely shelter, which carries a heavy weight in the CPI, show signs of heat. We expect it to keep inflation near or above 2% for some time. Therefore, once employment has made substantial progress the Federal Reserve is likely to take its foot off the monetary accelerator and start tapering asset purchases by year-end.”

Our Latest Analysis

Central bank interest in cryptocurrencies is rising. In our latest insight piece, we examine the current state of central bank digital currencies (CBDCs) and what they could mean for the economy.

We recently polled our network to examine the key risks to the U.S. economic outlook. See the results and our analysis here.