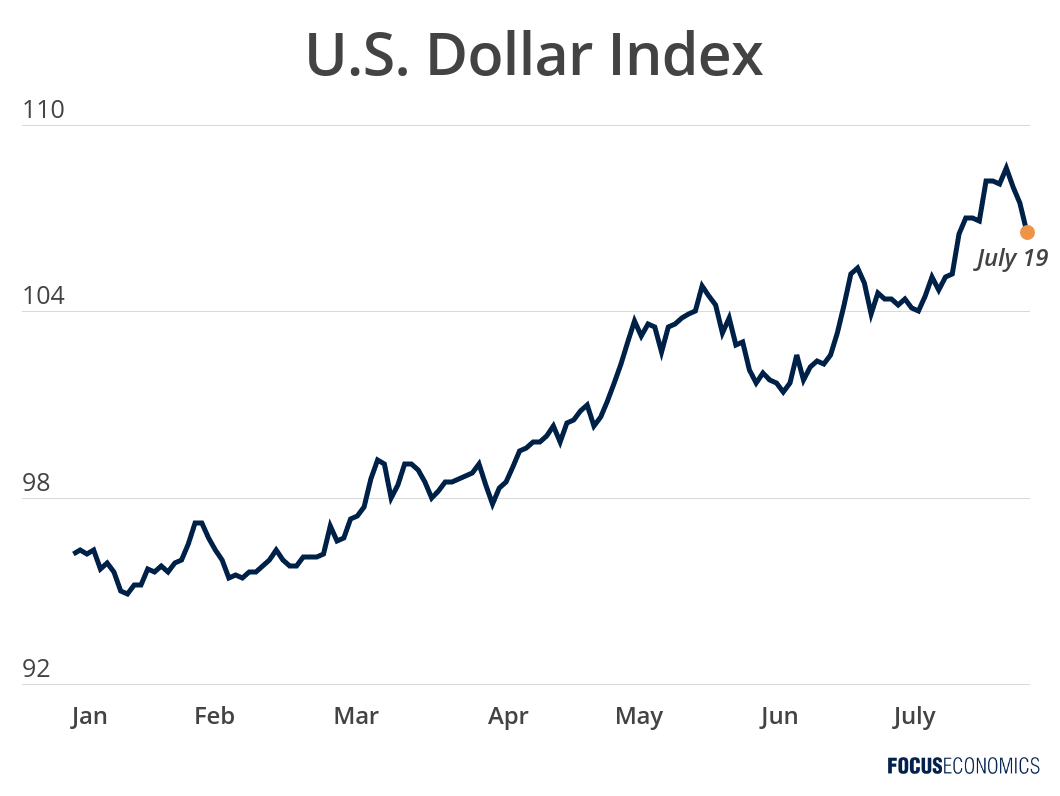

The USD is currently trading at its highest level in around two decades, with the currency close to parity with the euro and the trade-weighted U.S. dollar index up over 10% so far this year. Aggressive monetary tightening by the Fed has been an important factor behind the appreciation. Safe-haven demand—due to the Russia-Ukraine war, China’s lockdowns and fears of a global slowdown—have also boosted the dollar. Multi-year high energy prices have played a further role, given the U.S.’ position as a net energy exporter.

The strong dollar is likely to be welcomed in the U.S., as it will aid the Fed in its fight against inflation. However, for other countries the opposite is true. Given that the U.S. is an important trading partner to many countries—and more importantly that international commodities are priced in USD—the stronger dollar leads to higher imported inflation in the rest of the world. This will likely force foreign central banks into unwanted monetary tightening, weighing on growth.

Moreover, the strength of the dollar increases the value of dollar-denominated debt of both companies and governments. In emerging economies, a substantial share of total public debt is denominated in dollars, as these nations’ shallow financial markets limit the possibility for raising capital domestically. The stronger dollar also weighs on the current account by raising the import bill, and has thus been a factor behind the ongoing balance of payments and public debt crises of developing countries such as Pakistan and Sri Lanka.

Our analysts currently expect the dollar to pull back from its current level by the end of the year. The relative pace of policy rate tightening between the Fed and the rest of the world, the health of the global economy and geopolitical developments—especially linked to the war in Ukraine—will be key to watch.

Insights from our analyst network:

On the prospect of dollar weakening ahead, analysts at ING commented:

“Sustained dollar depreciation will need to be accompanied by a significant stabilisation and some recovery in global risk assets. That may still prove challenging in a high-interest rate environment, and while markets continue to deal with the incumbent threat of a global recession. Our view is that even if the dollar did bottom out in the past week, the path to a sustained depreciation remains challenging, and would most likely be very gradual from this point on. And risks of other rounds of dollar strengthening remain very elevated.”

On the euro, Desjardins said:

“The euro recently fell to parity with the US dollar for the first time since late 2002. It’s underperforming for a number of reasons. First, the greenback remains strong against most currencies because it’s a safe haven in uncertain times. Second, the European Central Bank (ECB) is lagging behind with its monetary tightening. Third, recession seems more likely in Europe due to increasing natural gas supply issues and other effects of the war in Ukraine. Finally, there’s concern about the ECB’s upcoming rate hikes and how they could affect some eurozone countries […]. We still think investor risk appetite will remain soft over the coming quarters, continuing to support the US dollar. We’ll be watching the euro for renewed sovereign debt tensions.”